Why do landlords need pay stubs for apartment applications?

Renting in today’s competitive markets depends on clear, credible proof of income. Landlords and property managers ask for recent pay stubs to confirm you can meet rent obligations. This guide shows how to create pay stubs for apartment applications the right way—by organizing the payroll records you already have.

Last updated: September 2025

At FinancialDocsProvider.com, we focus on formatting and presenting your authentic documents. We never invent numbers, dates or employers. Our role is to make your records easy to read and simple to verify. In the pages below, you’ll learn the legal basics, which edits are permitted, which are prohibited, and how to package your pay stubs so landlords, lenders and underwriters can quickly say “yes.”

Related Entities & Terms

- Pay stub / payslip / payroll statement / remittance advice

- W‑2 and 1099 (US); P60, P45, SA302 (UK); T4, T4A, Notice of Assessment (NOA) (Canada)

- Gross vs net pay, year‑to‑date (YTD) totals, variable vs fixed deductions

- Employer Identification Number (EIN), Social Security number (SSN), National Insurance (NI) number, Social Insurance Number (SIN)

- Regulators: CFPB, FTC & IRS (US); HMRC & FCA (UK); CRA & FCAC (Canada)

- Bank statements, employment verification letters, profit and loss statements, tax transcripts

- Direct deposit, payroll providers (ADP, Paychex, Gusto), PDF/A conversion, OCR and metadata cleanup

- Underwriting, income verification, affordability assessment and fraud detection

What are the legal basics of pay stubs for apartment rentals?

Pay stubs are regulated wage statements, not just receipts. When you create pay stubs for apartment packages, the content must mirror your employer‑issued data. In the US, UK and Canada, rules require itemized details that show how gross pay becomes net pay.

By law, a pay stub should display pay period dates, gross pay, deductions and take‑home pay. The CFPB explains that gross income is total pay before deductions, YTD totals show cumulative earnings, and net income is the amount you actually receive. UK guidance echoes this, requiring payslips to show gross wages, deductions, net wages and hours worked if pay varies. In Canada, employees access secure portals for official stubs used to confirm earnings and deductions.

Keep the distinction between formatting and falsification front and center. Formatting covers layout, redaction, file conversion and bundling documents. Falsification is any change to amounts, dates, names or employers that misrepresents reality. The IRS advises taxpayers responding to income verification requests to provide copies of multiple pay statements, not just a W‑2. Misstatements can lead to eviction, denial of credit, and potential criminal liability under US, Canadian and UK law.

- Core elements to capture: employer name and address; employee name and address; pay period; pay date; hours or salary basis; gross pay; itemized deductions; net pay; and YTD totals.

- Consistency matters: the same legal name should appear across stubs, bank statements and your rental application.

- Traceability: deposits shown on bank statements should reconcile to amounts shown on the stubs.

Which edits are allowed?

Edits that improve clarity and privacy—without changing facts—are acceptable. Well‑formatted documents reduce questions and speed decisions. Permitted edits fall into three buckets: privacy, readability and technical fixes.

Privacy edits

Mask or redact sensitive identifiers such as full Social Security numbers, National Insurance numbers and bank account details. Landlords do not need this data to verify income. Leaving the last four digits where possible helps confirm authenticity while protecting you from identity theft.

- Black out full SSN, NI or SIN; leave the last four digits.

- Redact direct‑deposit account numbers and routing numbers.

- Remove QR codes or barcodes that expose payroll portals.

- Add a small “Redacted Copy” note to avoid confusion.

Readability edits

If the original stub is hard to read due to faint print or poor scans, re‑typesetting for legibility is fine. You can align columns, add clear headings, adjust contrast and remove blank pages. Translation notes are also acceptable when presenting non‑English payslips to an English‑speaking reviewer.

- Recreate tables with consistent alignment and column labels.

- Fix rotated pages, skewed scans and cut‑off margins.

- Add a short glossary for common terms if your stub is in another language.

- Attach a one‑page cover sheet summarizing pay frequency and deposit timing.

Technical edits

Many applicants combine multiple stubs into a single PDF to streamline submissions. Converting images to PDF/A for long‑term storage, compressing file size, rotating pages and adding bookmarks are all allowed. Metadata cleanup—removing device details or geolocation tags—is a smart privacy step.

- Merge the last three pay stubs into one bookmarked PDF.

- Convert photos to PDFs and normalize page sizes for a tidy package.

- Strip author and GPS metadata from exported files.

- Use file names that make sense (e.g., “2025‑08‑30‑Stub‑ABC‑Corp.pdf”).

All permitted edits share one rule: they do not change the numbers or facts. Gross pay, deductions, net pay, dates, employer details and YTD totals must remain exactly as issued. When in doubt, add supporting bank statements or an employer letter.

What edits are illegal?

Any change that alters factual content crosses the line into fraud. Inflating wages, erasing deductions, modifying pay dates, or changing employer details is prohibited. Fabricating an entire stub is likewise fraudulent.

Regulators treat falsified financial documents seriously. In the US, misrepresentation to obtain housing or credit can trigger federal fraud charges. In the UK, the Fraud Act 2006 penalizes dishonest false representations with substantial penalties. In Canada, income misrepresentation may violate the Criminal Code. Reviewers often cross‑check stubs against bank deposits, employer letters and credit files. The IRS notes that acceptable documentation includes copies of multiple pay statements—if amounts don’t match, expect rejection.

- Do not: change hours, rates, bonus amounts or overtime figures.

- Do not: shuffle dates to make old stubs look current.

- Do not: replace an employer name or address to hide job changes.

- Do not: edit tax withholdings to inflate net pay.

If your income is insufficient for a specific unit, explore alternatives like a co‑signer or an apartment with different qualification thresholds. FinancialDocsProvider.com will not alter figures and will refuse any request that involves misrepresentation.

When do you need professional document formatting?

Sometimes a quick photo of a pay stub isn’t enough. Professional formatting adds value when clarity, consistency and compliance are essential. Here are common scenarios where a polished package can accelerate approvals.

Apartment and rental applications

Most landlords request two or three recent stubs. If your earnings vary, or your employer’s template is confusing, a consolidated, standardized package can help. For example, a nurse working variable shifts may receive separate stubs for base pay and overtime. We merge them, standardize the layout and make gross pay, deductions and net pay unmistakably clear for property managers.

- What reviewers look for: consistent names, stable YTD growth, and deposits that match net pay.

- Smart add‑ons: a brief cover sheet noting pay frequency and whether overtime is regular or occasional.

- Optional proof: 60–90 days of bank statements with corresponding deposits highlighted.

Mini‑scenario: You changed employers last month. Your package should include the final stub from Employer A, the first two stubs from Employer B, and bank deposits that tie to both. A short note explaining the transition timing keeps reviewers oriented.

Auto loans, mortgages and SBA financing

Lenders often compare stubs against bank statements and tax forms over longer periods. We help employees compile W‑2 forms, pay stubs and deposit summaries. For contractors, we pair 1099 forms, invoices and an income summary. Our cross‑checking guide explains how underwriters reconcile figures to deposits.

- Typical bundle: 30–60 days of stubs, two months of bank statements and the most recent W‑2.

- For variable pay: show base pay, overtime or commissions on separate lines with clear legends.

- For recent raises: include HR confirmation or a letter explaining effective dates.

Self‑employed and gig workers

Freelancers and gig workers rarely receive traditional stubs. Instead, they use invoices, 1099‑NEC (US), SA302 (UK), or NOA/T4A (Canada). We assemble an organized packet with invoices, bank statements and a simple profit‑and‑loss summary, all formatted consistently. A graphic designer renting an apartment might provide three months of invoices and a bank reconciliation; we combine these into a cohesive PDF with a cover sheet describing pay cadence and average monthly income.

- Proof stack: invoices, 1099‑NEC or T4A slips, bank deposits, and a P&L summary.

- Labeling: annotate transfers between accounts to avoid double‑counting income.

- Context: explain seasonality or large one‑off projects in a single paragraph.

Other common use cases

- Visa and immigration applications: embassies often require proof of ongoing income. Professionally formatted stubs paired with tax returns help officers understand your situation quickly.

- Government benefits: housing vouchers or social services may ask for current payslips and employment confirmation.

- Business credit: small‑business lenders may ask for the owner’s personal income documentation alongside corporate financials.

No matter the scenario, the objective is the same: present real numbers in a clear, consistent, and verifiable way. Our article on pay stubs versus paychecks explains why stubs carry more detail for underwriters than paychecks alone.

How does FinancialDocsProvider.com work?

We follow a structured, compliance‑first process designed to deliver polished documents without changing facts. Here is what the engagement looks like from intake to delivery.

- Secure intake: upload your pay stubs, tax forms and supporting documents through our encrypted portal. We never ask for passwords or logins and adhere to data‑privacy regulations.

- Reconciliation: we review each document for alignment across pay periods, amounts and totals. If we spot a discrepancy—such as a YTD figure that doesn’t match pay frequency—we flag it and offer guidance.

- Formatting and redaction: we clean the layout, align columns, add clear headers and redaction, convert images to PDF/A and merge multiple stubs into a single file when helpful.

- Quality review: a second specialist checks every figure against the originals. We run spell‑check and confirm the final package meets common lender and landlord requirements.

- Delivery: you receive a secure download link to your formatted documents. Standard turnaround is 24–72 hours depending on volume, with expedited options available.

We stay within legal and ethical boundaries at every step. We do not fabricate numbers or “doctor” documents. For proof‑of‑income editing, visit our services page for details, and review our pricing to plan ahead. To discuss your needs, please contact our team.

What belongs on your compliance checklist?

A strong pay stub package anticipates reviewer questions and makes verification simple. Use this checklist to validate completeness, clarity and consistency before you press “submit.”

- Identify yourself: use your legal name and current address consistently across stubs, bank statements and the rental application.

- Include employer details: stubs should show the employer’s legal name and address. If you have multiple jobs, keep stubs separate and clearly labeled.

- Confirm pay period dates: each stub must show the start and end dates of the pay period, along with the pay date.

- Verify gross and net pay: confirm calculations and ensure amounts match deposits. The CFPB guide explains how gross and net pay relate.

- Check YTD totals: year‑to‑date figures should move logically with each pay period. Inconsistencies signal errors or potential fraud.

- Show deductions: itemize taxes (federal/state or national insurance contributions), retirement contributions and benefits premiums. UK guidance requires gross wages, deductions and pay after deductions on payslips.

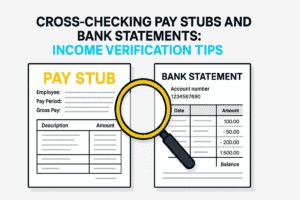

- Match bank statements: include statements that show deposits corresponding to each stub. Our cross‑checking article explains why this matters.

- Bundle supporting documents: include W‑2s, 1099s, T4s, NOAs or an employer verification letter, where applicable.

- Maintain legibility: ensure clear scans, no handwriting over figures, and complete pages without cut‑offs.

- Protect privacy: redact full SSN/NI/SIN and account numbers; keep the last four digits visible where feasible.

- Keep a paper trail: retain originals and maintain a folder with source files in case a reviewer requests them.

Completing this checklist before submission demonstrates professionalism and reduces back‑and‑forth. If you need help preparing the package, learn about our process.

What red flags lead to pay stub rejections?

Reviewers look for inconsistencies and signs of tampering. Avoid these common red flags to keep your application on track and minimize follow‑up requests.

- Mismatched fonts or alignment: inconsistent fonts, spacing or margins suggest manual editing.

- Unrealistic rounding: identical gross amounts every period (e.g., exactly $2,500.00) can look fabricated.

- Inconsistent dates: overlapping pay periods or missing weeks raise authenticity questions.

- Missing employer information: absent company names, addresses or tax IDs are a major warning sign.

- YTD totals that don’t add up: YTD earnings lower than the sum of reported pay periods indicate errors.

- Deductions that exceed gross pay: calculation mistakes or altered figures will trigger a denial.

- Poor image quality: blurry or pixelated scans can obscure details and delay decisions.

- Names or addresses that don’t match: if your stub lists an old address or nickname, provide a brief explanation or updated documentation.

- Metadata inconsistencies: conflicting PDF creation dates or software tags can hint at editing; use professional tools to clean metadata.

Our article on fake pay stub legal consequences explains these signals in more depth. If something looks “off,” underwriters will verify it. The cost of being caught far outweighs any short‑term benefit.

Where can you find official resources and further reading?

Staying informed helps you stay compliant. These official resources outline what must appear on a payslip and how to read it, plus guidance on documentation for verification.

- CFPB pay stub basics – a clear guide explaining gross income, deductions, YTD totals and net income.

- GOV.UK payslip guidance – explains that employers must issue payslips showing gross wages, deductions and pay after deductions.

- IRS documentation guidance – notes that acceptable documentation includes copies of at least three pay statements or check stubs.

- Cross‑checking pay stubs and bank statements – our internal article on reconciling income documents.

- Pay stub vs paycheck – understand why pay stubs carry more detail than paychecks.

- Fake pay stub legal consequences & rejection risks – learn the pitfalls of falsifying documents.

- Real customer stories – see how proper formatting helped applicants get approved.

- For proof of income editing and document formatting services, visit our services page and review our pricing.

FAQs

How many pay stubs should I submit for an apartment application?

Most landlords and property managers ask for at least two or three recent pay stubs to confirm steady income. Some may request more if you are self‑employed or have variable earnings. Always follow the application instructions and include bank statements that show the matching deposits.

Are online pay stub generators legal for rental applications?

Online generators can be legitimate when used to recreate your existing payroll data in a cleaner format. Using a generator to fabricate income or employment is illegal and can result in rejection or criminal charges. Base any generated stub on actual payroll information and keep amounts, dates and employer details accurate.

What should I do if I am self‑employed and need pay stubs?

If you don’t receive traditional pay stubs, assemble a proof‑of‑income packet with invoices, 1099‑NEC (US), SA302 forms (UK) or NOA/T4A slips (Canada), plus corresponding bank statements. A simple profit‑and‑loss statement showing income and expenses can also help. We can format these into a cohesive PDF for your landlord or lender.

Can I edit the format of my pay stubs for clarity?

Yes. You can remove blank pages, align columns, translate non‑English terms and redact personal identifiers without changing numerical data. The goal of editing is to improve readability and privacy—not to alter facts. Any change to amounts, dates or employers would be considered fraud.

Why do landlords compare pay stubs to bank statements?

Landlords want to confirm that the income shown on your stubs actually reaches your bank account. Comparing stubs to deposit records helps them detect inconsistencies or potential fraud. Providing recent bank statements alongside your stubs speeds verification and builds trust.

Need accurate, reliable financial documents fast? Contact FinancialDocsProvider.com now.

About the author: This article was written by the FinancialDocsProvider.com editorial team. Our experts specialise in compliance‑first editing, formatting and reconciliation of pay stubs, bank statements and tax documents for renters, loan applicants and business owners. Learn more about our process.

2")

Add comment